Restaurant operators feel it in the nightly closeout: fewer tables order a second round, and more guests skip alcohol altogether. The bar still matters—but alcohol no longer carries the same automatic weight on the P&L.

What are operators doing about it? They aren’t replacing alcohol with water, they’re replacing it with premiumized non-alcoholic (NA) drinks that can hold price, drive attachment, and keep the bar relevant. SpotOn menu data from independent restaurants shows exactly how they’re doing it.

From January 1, 2025 through February 15, 2026, SpotOn clients added 179.4 new beverage items per 100 restaurants. New beverage items were concentrated in three clear lanes: “Treat” beverages like refreshers and dirty sodas, zero/low-proof options like mocktails and NA beer, and functional drinks built around herbal, gut-health, and wellness cues.

This isn’t cultural commentary. It’s margin defense. The operators winning right now are the ones turning non-alcoholic beverages into a real menu category instead of an accommodation.

Key Findings

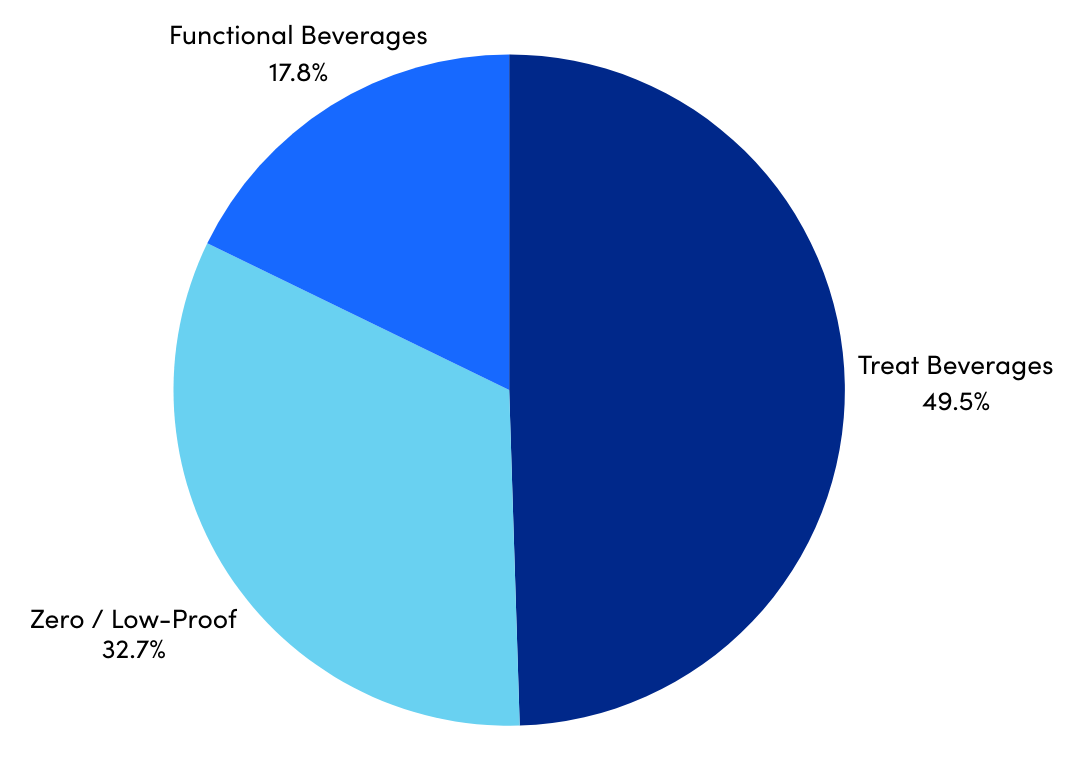

Across a sample size of 1,000+ independent restaurants, SpotOn reports 1,952 net-new NA beverage menu additions between Jan 1, 2025–Feb 15, 2026, or 179.4 additions per 100 restaurants concentrated across three main categories: Treat, Zero/Low Proof, and Functional Beverages.

- Treat beverages are now the primary growth engine: Making up the largest category (49.5%) encompassing various refreshers and dirty sodas.

- Zero/low-proof beverages are becoming the anchor, moving from “mocktail” to full program: With 32.7% of additions including mocktails, NA beer and wine, and other zero-proof beverages.

- Functional beverages are a meaningful third lane with premium add-ons and all daypart applications: With 17.8% of additions using phrases like adaptogenic, calm, fresh-pressed, herbal, immunity, probiotic or prebiotic, and wellness made up the remaining. *Note: Functional beverages were identified using menu naming which may undercount items that deliver benefits without explicit claims in their names.

Why NA beverages are now a profit strategy, not a compromise

The shift toward non-alcoholic beverages isn’t a single trend. It’s three consumer behavior demand changes showing up at the same table. Together, they explain why independent restaurants are moving NA drinks from a “mocktail option” to a real profit category.

- Occasions are changing with fewer default drinkers: Operators are serving more groups where some guests drink alcohol and others don’t, and everyone still wants to feel included. This is especially true as Gen Z and Millennials account for a larger share of dining occasions and drink less alcohol than older cohorts. The opportunity is that GenZ still over-index on beverage purchasing behavior and are more likely to order a drink, just not necessarily a drink with alcohol. That increases the need for a beverage ladder that feels social and celebratory for every guest at the table.

- Value-seeking indulgence is rising with guests seeking small luxuries: In a price-sensitive environment, diners trade down from bigger-ticket items but still reward themselves. That’s why treat beverages including refreshers and dirty sodas are driving so much menu innovation. They deliver an affordable indulgence with high perceived value, fast execution, and strong margins. For operators, these drinks can help replace some of the lost “second round” energy with options that feel fun, instagrammable, and upgradeable without the complexity of a full cocktail build.

- Wellness is becoming a driver with moderation, health cues, and GLP-1 influencing behavior: Wellness is no longer niche. Guests are increasingly responsive to cues like herbal, gut health, and immunity; and more cautious about alcohol overall. At the same time, an uptick in GLP-1 usage is influencing restaurant behavior, often reducing cravings for high-calorie items and alcohol, while increasing spending in restaurants offering healthier, smaller-portion and non-alcoholic options. The operational implication is direct: when alcohol demand softens, guests don’t stop ordering beverages. Instead they shift toward options that align with how they want to feel. Functional and zero/low-proof drinks help operators protect beverage attachment while meeting a new definition of “worth it.”

Bottom line for operators? These drivers all point to the same play. Operators that treat non-alcoholic beverages as a profit strategy designed for occasion, indulgence, and wellness are best positioned to keep the bar relevant even as alcohol becomes less automatic.

A deeper dive into each category

Throughout the timeline, NA beer and mocktails remain the workhorses of a traditional NA beverage program, but they play different roles with NA beer often serving as a social utility, while mocktails, zero-proof cocktails, and treat beverages present an experience.

Treat beverages: refreshers lead with dirty sodas on the rise

In an uncertain economy, consumers opt for littler luxuries. Refreshers and dirty sodas deliver margin for operators while offering consumers an affordable indulgence.

Treat beverages take up the biggest slice of the new category mix at 49.5% with refreshers making up 85% of the treat beverage category. Dirty sodas are still growing at 15% but show momentum with SpotOn reporting February 2026 dirty soda additions exceed January 2026 additions.

Refresher items skew heavily toward flavor-led using house-specialty drink language like the Kiwi Berry Refresher at Train Wreck Bar & Grill (Burlington, WA) and an array of Refreshers at Fat Zach’s Pizza locations across Washington state. Refreshers are built as riffs on a classic like lemonade, tea, or juice, with some even touting energy add-ons.

Dirty soda offerings are largely soda-based with mix-ins like flavored syrups and creams like the Under the Sea Dirty Soda at Marble Coffee Co. (Billings, MT) and the Dirty Cupid and Dirty Shirley at The Pit-Stop (Stockton, IL).

Zero/Low-proof goes beyond mocktails

SpotOn found the most common formats of NA beverages were zero-proof cocktails/spirits (65.2%), mocktails (19.9%), and NA beer (10.2%). While NA wine/sparkling represents a smaller share (4.7%) these offerings remain important, especially for celebrations and special occasions.

Packaged vs. house-made

Independent operators often start with packaged non-alcoholic offerings before investing in a full program. This approach reduces training burden and prep complexity while still providing guests optionality. SpotOn data suggests many operators are building the foundation first, then leveling up. Interestingly, 64.6% of zero/low-proof additions were house-made or menu-described, while 35.4% are packaged and ready-to-sell.

- Packaged, ready-to-sell zero/low-proof items require less labor and make execution easier (buy, chill, pour). Of the packaged options: 28.8% are NA beer, 13.3% are NA wine, and a majority 58.0% fall into other packaged options, including canned beverages.

- When it comes to NA Beer, SpotOn found restaurants carrying options from mainstream breweries like Corona, Guinness, and Lagunitas to more niche brands like Athletic Brewing, Industrial Arts Brewing Co, Free Wave Hazy IPA, and Urban Artifact’s Seedless line.

- In the wine space, Crush'd Wine Bar & Kitchen (SF Bay Area) offers NA Chardonnay and Sparkling Rose from Leitz Weingut known for their highly regarded, premium NA wines under the Eins Zwei Zero label. Other NA wine options appearing on menus include Noughty Sparkling Rosé and TÖST Sparkling Rose.

- House-made zero/low-proof drinks give operators more flexibility to create signature drinks that can be priced closer to cocktails. Of the house-made options: 46.1% are zero-proof labeled items, 30.8% are mocktails/NA cocktails, and 23.1% are other NA items.

- In the Mocktail category, SpotOn found a frozen mocktail lineup at La Hacienda (FL), a rotating Monthly mocktail special at The Barnyard Crafthouse & Kitchen (Tucson, AZ), and a full mocktail lineup featuring a Spritz, Mule and more at Balsamico Italian Kitchen in San Diego.

- Zero-Proof Items typically refer to more sophisticated options that use non-alcoholic spirits, shrubs, and other premium ingredients.

- Other NA options include Key Lime and Spice Pear Slushies from Bona Fide Deluxe (Atlanta), a Thai Coffee Affogato at Thai Papaya Garden (Dallas), and multiple instances of Butter Beer, typically a blend of cream soda, toffee or caramel, and heavy cream; sometimes with butter or butterscotch.

- SpotOn also found a growing number of NA spirits including Ritual Zero Proof (gin, rum, tequila, whisky, agave).

Functional beverages: herbal dominates, but probiotic/prebiotic spikes

Restaurants are not just adding “NA options,” they’re adding benefit-focused drinks to address gut health, immunity and overall wellness using consumer-recognizable retail formats like teas, shots, kombucha, prebiotic sodas and more. SpotOn found operators largely opt to add more mainstream options like herbal tea that signal comfort and ritual and probiotic/prebiotic sodas that address gut health, while buzzier items like “adaptogenic” are less popular.

Functional beverage additions break down with 46.3% Herbal, 21.6% Probiotic/prebiotic, 12.4% Immunity, 8.9% THC, 8.6% Wellness, 1.7% Calm and just 1% adaptogenic.

The Book Worm Cafe (Dayton, OH) offers Immunity Booster and Mushroom Immunity Shots, while Killer Queen Wine Bar (Durham, NC), Salt-N-Pepper Sandwich & Grill (San Francisco, CA) and Black Cap Coffee & Bakery (Stowe, VT) have added gut-healthy sodas from CulturePop, Poppi, and TreTap to their menu. SpotOn also observed an emerging set of THC beverages with notable clustering in parts of North Carolina.

Seasonality: Dry January evolves into a roadmap

Non-alcoholic beverage innovation no longer spikes for a single month. SpotOn data suggests January serves as a kick off, a predictable moment when operators add new NA items, tests to find what works, and build a program for the rest of the year. In fact, SpotOn found restaurants added 47% more NA items in January 2026 vs. January 2025 with the lift driven by zero/low-proof (+33%) and functional (+41%) additions.

From there, the pattern looks less like a one-off promotion and more like an occasion-led calendar, with different NA formats peaking when guests’ needs change:

Winter: Reset & celebration

Wellness and moderation cues rise in January, making it a high-impact window for both zero/low-proof and functional launches. A second wave follows in February as operators lean into “celebration without alcohol” opportunities to serve Valentine’s and date-night occasions. SpotOn data showed NA wine/sparkling saw the strongest additions in February. Zero/low-proof also shows early-year strength, peaking in February 2025.

Spring: Refresh & functional

As weather warms, menus move toward bright, flavor-forward “treat” options and benefit-led add-ons. SpotOn saw treat beverages peak in March 2025 with elevated activity through spring/early summer, while functional options peaked in April 2025, a natural fit with “clean start” consumer behavior.

Summer: Cooling, craveable, repeatable

Mocktails and refreshers show warm-weather strength with mocktails spiking in April 2025 and June 2025. Zero/low-proof also shows another peak in June 2025. This is prime season for LTO rotations: same base, new flavors, minimal complexity.

Fall: Largely a sports utility

NA beer behaves like an all-season utility item with noticeable upticks in September aligning with football season and Oktoberfest and November championship season and the start of NBA and NHL. NA beer stands out less as experience and more as social lubricant, a low-friction order for groups.

Holiday season: group-friendly inclusivity

November and December show spikes in general NA additions, suggesting operators anticipate large parties and mixed-preference groups. This is when optionality matters: something celebratory, something indulgent, and something “better-for-you.”

One signal to watch: Functional’s fastest acceleration is coming from gut health language. The sharpest January year-over-year change in functional beverages was probiotic/prebiotic items (+2400% from Jan 2025 to Jan 2026), a sign that operators are moving beyond “herbal tea” into more retail-based formats like prebiotic sodas and kombucha.

Seasonality isn’t just when to promote, it’s how (and when) to refresh or rotate the menu. January sets the foundation with zero/low and functional beverages, spring and summer drive repeat orders of treat + mocktail rotations, fall supports occasions with NA beer utility, and holidays reward inclusive menus that work for all consumers.

On the map: the NA boom is national

Non-alcoholic beverage growth is no longer limited to coastal metropolitan markets. SpotOn menu data shows independents across the country are actively building NA programs, but finds regions lean into different focuses within the category.

Treat Beverages skew Midwest first: Treat drink additions are most concentrated in the Midwest (37%), followed by the South (23.4%), Northeast (22.6%) and West (17.1%). This points to strong demand for affordable, flavor-forward indulgences with refreshers and dirty sodas.

Zero/Low-Proof broadly in demand with the Northeast leading the charge: Zero/low-proof additions are more evenly spread led by Northeast (26.5%), followed by then the West (24.9%), South (24.3%) and Midwest (20.8%). This widespread adoption suggests moderation and bar-style NA are becoming more commonplace throughout the U.S.

Functional shows a similar national footprint: With the Northeast (27.3%) slightly ahead of the South (25.6%), West (23.9%), and Midwest (23.3%), indicating wellness-led beverage demand is now a mainstream behavior.

SpotOn also found “hot spots” where the broad NA Categories is growing the fastest:

- New York Metro stands out for zero/low-proof and functional beverages, signaling a market where NA additions are moving beyond simple mocktails and into more comprehensive programs.

- Chicago appears across all three categories, particularly in functional, suggesting a wider adoption and a market where NA innovation is becoming routine.

- Los Angeles and the San Francisco Bay Area lead in zero/low-proof and functional options, consistent with markets that tend to lead in premium and wellness-driven consumption.

Its clear demand for non-alcoholic beverages has become widespread, but the winning format varies by region and customer. For operators in the Midwest or with value-focused guests, consider Treat Beverages as a strong margin play. For those in the Northeast or serving more sophisticated customers, opt for premium Zero/Low-Proof or Functional beverage offerings that work with the concept.

What’s next for operators

As a profit partner, SpotOn’s guidance for operators is to follow the data. Non-alcoholic beverages are no longer an option and have become vital for independents to build check average and drive margin. Profitable restaurants will treat NA as a true beverage program with the same discipline they apply to cocktails with clear pricing, smart placement, fast execution, and seasonal rotation.

Build a real NA menu, not a catch-all: Build a drink program that earns margin, not just fills a glass. Create a dedicated NA section with 6-10 beverage offerings that tackle the three reasons: craveable treats, social and celebratory zero/low-proof drinks, and functional feel-good options. Every table should have an NA option that feels as curated as the rest of the menu. For inspiration, check out the curated NA menu section at Blacksburg Wine Lab (VA) featuring zero-proof cocktails using premium ingredients like maple-squash shrubs and elderflower, a phony negroni mocktail, NA wine options and even a zero proof flight.

Use treat beverages as the easiest margin win: Treat drinks are the fastest way to protect beverage dollars without adding bar complexity. Keep the build standardized: one base (lemonade, tea, soda), a few rotating flavors and optional upgrades like energy add-ons, cream float, boba/popping pearls, or salted foam. Run 2-3 LTO flavors per season, keep 1-2 staples year-round, and price them like specialty beverages, not fountain drinks.

Make zero/low-proof feel premium and intentional: Operators can win by offering both packaged “grab-and-pour” items for speed and consistency and house-made mocktails. Anchor the program with a few recognizable options, then add one or two showstoppers that justify cocktail-adjacent pricing.

Lead functional with familiar benefits and formats: Functional sells fastest when guests immediately understand the promise. Operators should prioritize three formats: a comforting herbal tea or tonic, a gut-health option like pre/probiotic soda or kombucha, and a low-prep, high perceived value shot/elixir. Keep the language consumer-friendly and avoid complications that might slow ordering.

Build a tiered beverage ladder: Give guests an easy way to trade up: house-made refreshers, premium treat builds, elevated zero-proof options, and functional add-ons. Be sure to train staff and arm them with a simple one liner “Looking for something fun without alcohol or something more wellness focused?

Engineer for speed and profit: Avoid operational drag from menu sprawl by building around shared bases, garnishes and glassware across beverage categories. Track sales mix by daypart and season, and refresh quarterly. The goal is a beverage program that looks plentiful to guests, but is easy to execute for staff.