No matter what you serve, where you’re located, or what your concept is, every successful restaurant business has one thing in common: steady cash flow.

But keeping money coming in isn’t easy. Both new owners and seasoned operators alike face unpredictable sales, rising costs, and the constant need to reinvest in their business—it doesn’t take much for things to get tight.

To keep things running smoothly, it takes capital.

That’s why so many restaurants turn to loans or other forms of financing to bridge the gap between expenses and long-term growth.

A loan can help you purchase property, buy equipment, or cover day-to-day expenses when revenue dips. But not all loans work the same way, and not every funding option requires a bank.

In this article, you will learn:

- The pros and cons of traditional loans, like bank and SBA loan options

- Flexible alternatives for newer or fast-growing restaurants

- How your POS can help you access capital faster, with less hassle

Let’s start by looking at traditional loan options—the ones that often come to mind first when restaurant owners think about funding and how they fit different business goals.

Traditional restaurant loan options explained

When most restaurant owners think about getting a loan, they picture sitting down with a bank or applying through the Small Business Administration (SBA).

These traditional loans can be great for restaurants with steady revenue and a strong balance sheet, but they often come with longer approval times and more paperwork than newer funding options.

Here’s how the most common traditional loans break down, and what you need to know before applying.

Bank loans

Bank loans are the most well-known form of financing in the restaurant industry. They typically offer the largest loan size and the lowest interest rates, making them ideal for established businesses planning to purchase property, expand to a new location, or refinance existing debt.

For example, a restaurant with a history of profitable operations might secure a $250,000 loan to build out a second location, or a $600,000 commercial real estate loan to purchase the building instead of leasing.

However, lenders often require strong credit, detailed financial statements such as P&L, and valuable collateral to secure the loan.

While the process can be slow, this option works well for restaurants with consistent cash flow and time to wait for approval.

Bank loans at a glance:

- Best for established restaurants with solid credit and consistent revenue

- Lower interest rates, higher loan amounts

- Requires financial documentation and collateral

- Slow approval process — not ideal if you need funds quickly

How to move forward:

Start with the bank where you already have a business account. Ask for a business loan specialist and request a list of required documents before applying.

SBA loans

SBA loans, also known as SBA-backed loans, are supported by the Small Business Administration and give restaurant businesses access to flexible loan programs with longer repayment terms and lower fees than most banks.

The catch is that you’ll need to meet specific eligibility requirements and submit extensive documents, from tax records to a detailed business plan. SBA loans are only available to restaurants that operate as a for-profit business, not nonprofits or charitable organizations.

For many operators, that level of red tape makes SBA options best suited for long-term financing, like renovations, construction, or expansion projects that can wait for approval.

SBA loans at a glance

- Lower fees and longer repayment terms

- Backed by the government, issued through lenders

- Requires extensive documentation and approval steps

- Best for larger projects that aren’t time sensitive

How to move forward:

Visit SBA.gov and use the lender match tool, or ask your current bank if they process SBA-backed loans.

Business lines of credit

A business line of credit is another reliable option for restaurants that need ongoing working capital rather than a single lump sum.

Once approved, you can draw funds as needed, say, to handle a sudden equipment failure or cover seasonal expenses, and only pay interest on what you use.

It’s very similar to a credit card, but with key differences:

- You can access cash directly without cash advance fees

- It usually has lower interest rates

- You can typically borrow higher amounts than a credit card allows

This flexibility makes lines of credit ideal for experienced operators looking to better manage their operations and smooth out revenue fluctuations.

Traditional loans can be powerful tools for established restaurants, but they’re not the only path to capital. If you’re new to the restaurant industry or need funds quickly, alternative financing might be a better fit.

Business lines of credit at a glance

- Flexible funding (only borrow what you need)

- Only pay interest on what you draw

- Helpful during slow periods or emergency situations

- Typically requires good credit and strong revenue history

How to move forward:

Ask your current bank or credit union whether they offer business lines of credit and what their minimum annual revenue requirements are.

Alternative funding for new and growing restaurants

Not every restaurant has the credit history or financial profile to walk into a bank and get approved. Newer operators or growing concepts often need faster, more flexible ways to access capital, especially when time and paperwork aren’t on their side.

Fortunately, there are several alternative funding options designed for restaurants in that exact situation.

Equipment financing

If you need to buy equipment, upgrade your POS, or repair equipment that’s critical to daily operations, equipment financing can be a smart choice.

The loan itself is backed by the equipment you’re purchasing, which helps keep interest rates reasonable and eligibility requirements manageable.

For many restaurants, this is one of the fastest ways to access funds without tying up other assets as collateral.

Equipment financing at a glance

- Ideal for replacing or upgrading essential equipment

- Equipment itself serves as collateral

- Fast approval compared to traditional loans

How to move forward:

Ask the equipment vendor whether they partner with lenders—they often have preferred financing relationships that speed up approval. If you use SpotOn, you can explore our POS equipment financing options and get approved quickly, so you can upgrade your equipment and keep business moving.

Not recommended: Merchant cash advances (MCAs)

Merchant cash advances may sound appealing; they offer quick access to money (usually within 24-72 hours) based on your future sales, but they come with major downsides.

These advances aren’t technically loans, which means they don’t follow the same repayment terms or transparency standards as other loan programs.

Yes, you can get funds quickly, but there are inherent drawbacks:

- High costs: MCAs often carry steep fees and factor rates that translate to extremely high effective interest.

- Frequent repayments: Most agreements require daily or weekly withdrawals from your account based on projected sales, and missing even one payment can trigger penalties or default clauses.

- Limited flexibility: Because repayments are automatic and tied to sales, it’s difficult to pause or renegotiate terms if business slows down.

Read our article Merchant Cash Advances: the Smoke & Mirrors Version of Small Business Financing to learn more about how MCAs work and reasons why you should avoid using them.

MCAs at a glance

- Fast funding (typically 24-72 hours)

- Not technically a loan

- Very expensive, with high fees and rigid repayment options

- Can rapidly strain cash flow

How to move forward

You shouldn’t. Steer clear of these loans completely.

Crowdfunding or investor partnerships

For restaurant concepts with strong branding or community support, crowdfunding platforms and investor partnerships can be creative ways to raise capital without going through a bank.

Just know that you may be trading speed or control for that money. Investors often want equity or a say in operations, and crowdfunding takes time and marketing to do well.

Still, when executed strategically, these approaches can align financial backers with your restaurant’s vision and growth goals.

Crowdfunding and investor partnerships at a glance

- No monthly loan repayments or interest

- Works best with a strong brand or loyal audience

- May require giving up equity or decision-making control

- Takes time and effort to pitch, market, and manage ongoing communication

How to move forward:

Choose a platform (Kickstarter, Fundable, etc.), then define what supporters get in return, and build your pitch around that story—not just your funding goal. Supporters need to know why your restaurant matters, what makes it different, and what they get by backing it.

Personal and startup loans

If your restaurant is still in the idea stage or hasn’t built business credit yet, personal loans or startup loans can be a bridge to get things off the ground.

While interest rates are typically higher and the loan size smaller than SBA-backed loans, they’re often easier to qualify for and faster to process.

Just make sure to borrow conservatively and have a clear plan for repayment once your restaurant’s revenue starts coming in.

Personal and startup loans at a glance:

- Easier qualifications for newer restaurants

- Higher interest rates and small loan amounts

- Your personal credit and finances are at risk

How to move forward:

Check with your personal bank or credit union first. They can often pre-qualify you without taking a hit to your credit score.

Now it’s time to figure out which restaurant loan is the best fit for your business. Just because you can qualify for a specific loan doesn’t mean it will help with your goals, cash flow, and timeline for growth.

A faster, simpler restaurant loan through your POS

If you’re like most restaurant owners, you don’t have time to fill out a 20-page application, dig up five years of financial statements, then wait weeks just to find out whether or not you’re approved.

That’s why some lenders now use data pulled directly from your POS to qualify restaurants automatically.

Instead of judging your business by your credit score alone, they analyze your actual sales and cash flow to determine your eligibility—giving you access to funds and repayment options that match how you operate.

Let’s go a little deeper into how this works.

Faster access to capital

Because your POS tracks every transaction, lenders get a clear picture of your restaurant’s revenue and cash flow. That allows them to make approval decisions quickly, often within a few days instead of weeks.

Once approved, the money goes straight into your account, and you can use it for anything your business needs, from working capital to staffing, marketing, or replacing critical equipment.

Repayment is flexible and simple

Instead of fixed monthly payments, POS loans are usually repaid through a small percentage of your daily credit card sales.

That means if business slows down one week, your payment amount adjusts with sales, giving your cash flow room to breathe. You’re not locked into rigid repayment terms that don’t reflect the ups and downs of real restaurant life.

SpotOn makes access to funds seamless

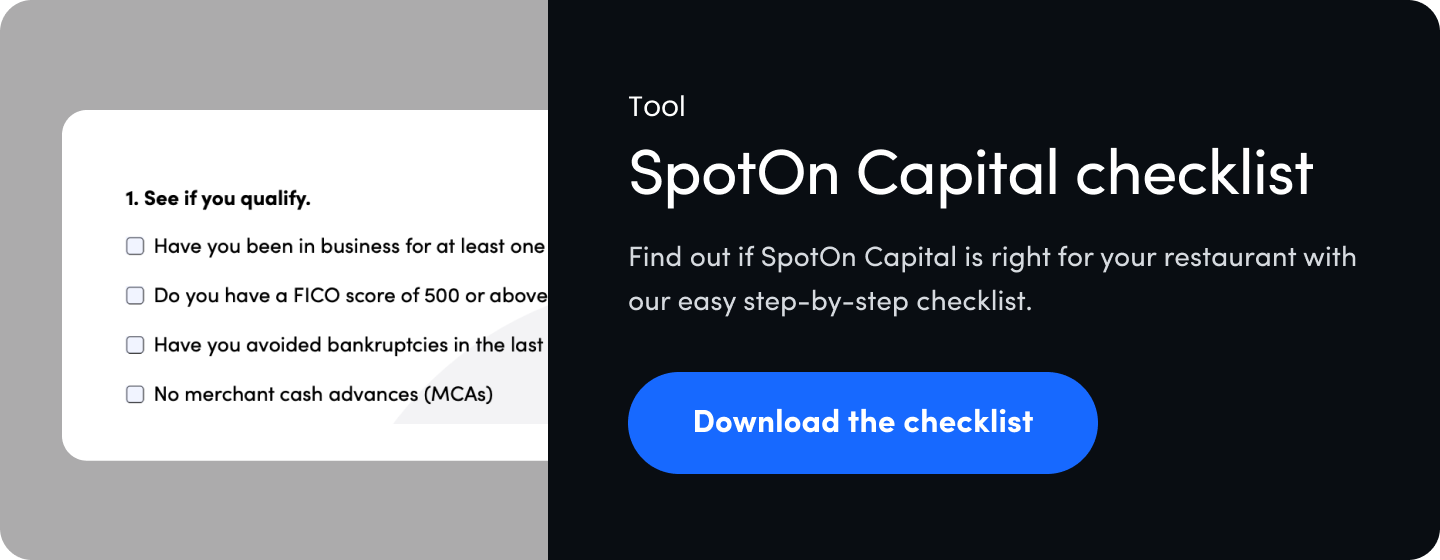

SpotOn Capital takes the same POS-based approach and turns it into a true business loan—with cash deposited directly into your account with no hidden fees or complicated terms.

Because SpotOn already processes your payments, the underwriting is nearly automatic, and qualified operators can receive funds in as little as one to two business days.

Repayments happen automatically through your POS with a single fixed rate—eliminating late fees and keeping everything predictable and stress-free.

It’s a straightforward, flexible system that fits your restaurant’s rhythm and keeps cash flow steady.

"SpotOn Capital has helped us tremendously to sustain our business, have cash flow, and do payroll." -Zach Johns

With a Capital loan from SpotOn, Fat Zach's got quick access to funding to pay for equipment and upgrades and pay it back from a percentage of daily sales.

How to choose the right funding for your restaurant

With so many loan programs and financing options available, the best choice depends on where your restaurant is in its journey and what you’re trying to accomplish.

It doesn’t matter if you’re looking for short-term working capital or planning long-term renovations; the right funding should align with your goals, your cash flow, and your ability to repay the loan comfortably.

Here’s how to narrow it down.

Match your funding to your business needs

Before you start filling out forms or talking to lenders, get clear on what you actually need the capital for:

- Are you trying to purchase property for a new location?

- Does your kitchen need a remodel?

- Is the slow season coming, and you need something to draw on to make ends meet?

Think of your funding as a tool: each option serves a different purpose within your broader business needs.

Compare repayment structures and timelines

A low interest rate might sound appealing, but the structure of your repayment terms often matters more.

Some loans require fixed monthly payments, while others tie repayment to your daily sales. Make sure you understand how the payback schedule affects your cash flow, especially during slower months.

When researching loan options, look for a lender that will give you a free quote upfront so you can understand the rough total cost before you apply.

Consider speed and simplicity

Ask yourself: how fast do I need the funds, and how much paperwork can I realistically handle?

Traditional banks and SBA options can offer favorable interest rates, but they usually require a deep dive into your financial statements and tax history.

If you need funds quickly or don’t have time to navigate layers of paperwork, look for financing options that streamline approvals and minimize red tape.

The goal is to find the right balance between speed, cost, and convenience so you can choose the funding option that makes the most sense for your business.

Before committing to any loan, use SpotOn’s free Break-Even Point Calculator to see how much revenue your restaurant needs to cover costs and confidently manage repayment. It automatically estimates your monthly, daily, and quarterly break-even points, helping you plan for profit before you take on new funding.

Frequently asked questions about restaurant loans

Looking for fast answers to questions about restaurant loans? Here are several answers to the most frequently asked questions.

What credit score do I need for a restaurant loan?

It depends on the loan, and every lender sets different eligibility requirements, but most traditional bank loans require at least a score of 680 or higher. Strong financial statements and steady revenue can also improve your odds of approval, especially if you’re seeking a larger loan size or better interest rates.

How long does it take to get approved for restaurant funding?

Approval timelines depend on the type of financing you choose. Traditional loans from a bank or the Small Business Administration (SBA) can take several weeks to process, while newer POS-based loan programs or equipment financing options may approve and deposit funds as soon as the next day.

What’s the difference between a loan and a merchant cash advance?

A loan is a formal financing agreement with fixed repayment terms, predictable interest rates, and clear fees. A merchant cash advance, on the other hand, is not a loan—it’s an advance against future sales, often with very high fees and no set repayment schedule. While it may offer quick access to money, it can put serious strain on your cash flow.

Can I get funding if my restaurant is new or has limited credit history?

Yes, but your options will likely look different. Startups and newer restaurants may not qualify for SBA-backed loans or bank financing, but they can often explore equipment loans, POS-based funding, or even personal loans. Having a clear business plan and solid revenue projections can help new borrowers demonstrate creditworthiness.

How does SpotOn POS funding compare to traditional loans?

SpotOn Capital offers a true business loan that’s faster and simpler to secure than most traditional loans. There’s no need for lengthy paperwork or multiple rounds of approval—SpotOn uses your POS data to assess your business performance, deposit funds directly into your account, and automate payments based on daily sales. It’s financing designed specifically for the pace of the restaurant industry.

DISCLAIMER: Everything here is just for informational purposes. The numbers, links, and graphics may not be accurate, and we encourage you to do your own research. Also, we can't guarantee results from following our advice. Always consult a professional for your specific situation.