A merchant cash advance, also known as an MCA, looks enticing at first glance. The promise? Fast, easy cash with no credit check. Okay, the fees are a bit higher. But what could possibly go wrong?

The reality? Exorbitantly high rates, personal and business liens, restrictive, loan-like covenants, numerous hidden fees, highly unregulated (resulting in abusive collection tactics), overwithholding, potential lawsuits… and financial ruin.

Unlike legitimate small business programs, like SpotOn Capital, MCAs are largely unregulated and often use deceptive marketing and sales tactics to appear like a good deal.

To help identify MCAs, let’s take an in-depth look at:

- What exactly MCAs are

- Mechanics of an MCA (aka how they make money at your expense)

- True cost of an MCA

- Better funding options available to you

Are you a new owner or manager still learning the ins and outs of running a restaurant as a business? Check out our free guide covering all the important basics for anyone interested in how to open a restaurant.

Merchant cash advances—an overview

Merchant cash advances purchase your business’ future receivables at a discount in exchange for a lump sum today.

While the creation of this funding option allowed businesses with thin or poor credit to bypass traditional lending criteria to access fast cash, it quickly became the “last resort.” Small businesses went to them because they had no other place to turn—hence an MCA’s very harsh terms.

Post–2008 financial crisis, banks tightened their commercial lending policies—and MCAs began pursuing borrowers who had better options available. Since then, they’ve earned their predatory reputation, with deceptive (and even illegal) marketing tactics—and lack of regulation to prevent the damage to small businesses—playing a large part in their spread.

Plenty of law firms specialize in MCA negotiation and lawsuit assistance for this reason.

Mechanics of an MCA

MCAs are neither federally regulated nor subject to state usury laws. This allows them to charge incredibly high interest rates (we’ve seen 581%) with no recourse for discrimination against protected classes. Also, they can (and often do) place a UCC lien on your business and personal property, allowing them to take it all when you default—as soon as the very first missed or disputed payment.

While not an exhaustive list, pay attention to these very important components making up your advance agreement.

How they make money:

1) FACTOR RATE

Factor rates are used to calculate the fixed fee added to your principal amount. For example, a $100,000 advance with a factor rate of 1.4 results in a $40,000 fee ($100,000 x 1.4 = $140,000). While factor rates are normal, MCA companies offer much higher factor rates.

2) ANNUAL PERCENTAGE RATE (APR)

MCA APRs are extreme, and they aren’t required to disclose this upfront.

3) ADDITIONAL FEES

You’ll see in the next section that MCAs often come with fees related to origination, administration, processing, late payment, legal, and even a fee to deposit your actual advance, which can add thousands to your total.

How they collect:

While repayment is made each day (some do weekly), even one missed payment can put you into default, triggering clauses like:

1) RECONCILIATION CLAUSE & PERSONAL GUARANTY

If included, a reconciliation clause allows you the opportunity to renegotiate the terms of your MCA. Renegotiation is not guaranteed, however, and often requires an attorney, which means you now pay legal fees to help reduce your MCA fees. And, this needs to be done before the MCA company files liens, lawsuits, and seizures against you—which your personal guaranty clause gives them the right to do, to both personal and business assets. This will also cost you plenty in legal fees—yours and the MCA company’s. Note: this is not the same as overwithholding.

2) CONFESSIONS OF JUDGEMENT

Not all states permit these; in those that do, you’re agreeing to be held liable in advance, allowing the company to obtain a judgment against you—often without notice or even a hearing.

The true math of a merchant cash advance

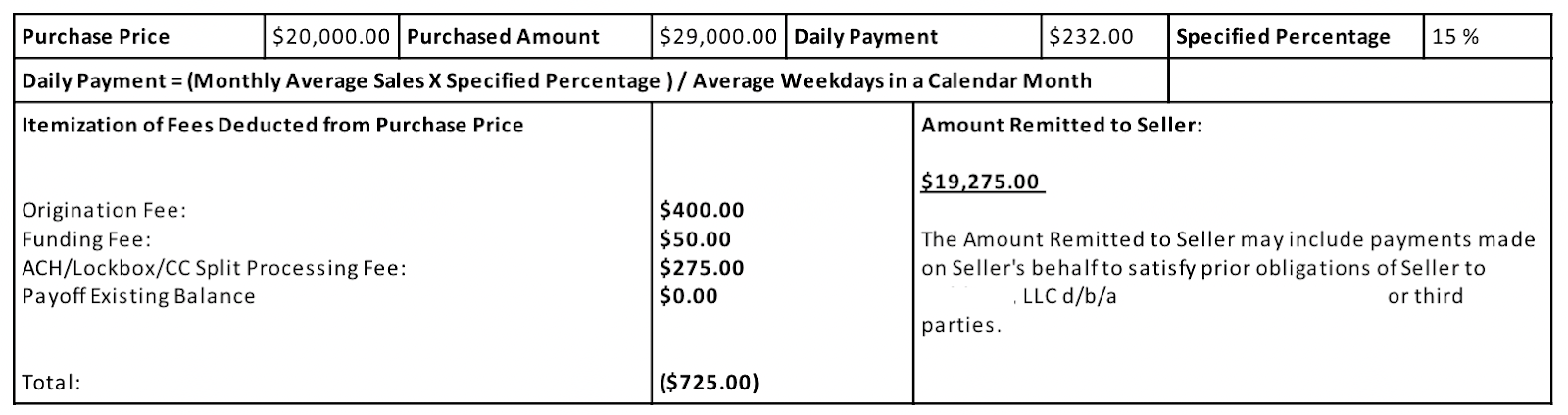

Here’s just one example of a typical MCA agreement for a hypothetical borrower, Samantha:

Samantha has a principal amount of $20,000, with a fee of $9,275 on the top, for a total of $29,725 owed—almost 50%. She’ll also pay almost $1,000 for tasks like funds deposit, processing her application, ACH withholding, and more—before she even receives her advance.

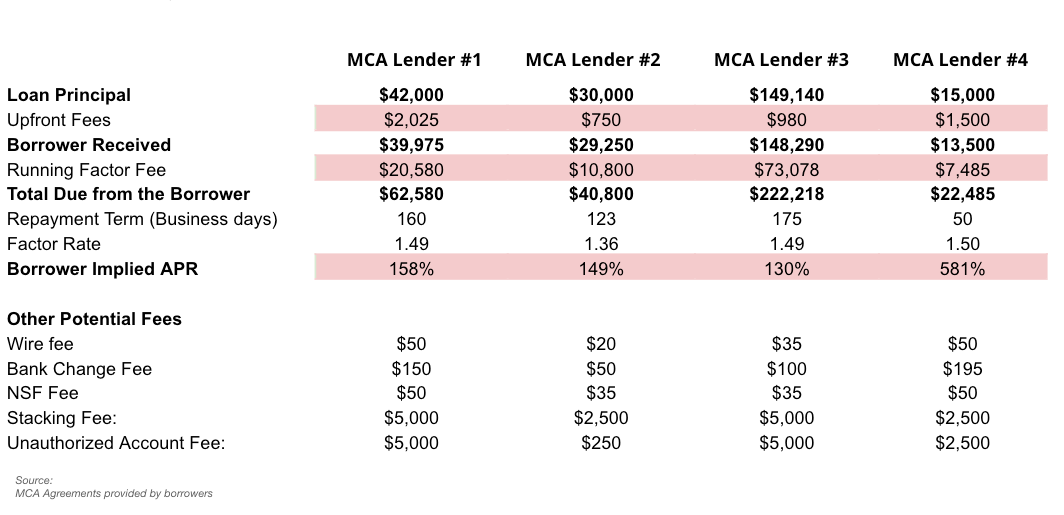

Below is a comparison of actual MCA company fees:

A note on overwithholding (“true up” clause)

Here’s another potential trap waiting for Samantha:

MCA companies often encourage applicants to overstate their daily or monthly sales in order to get more money. What you don’t realize when doing this, however, is that doing so proportionally increases your daily repayment. If sales slow down, that can spell disaster very quickly.

For example, Samantha makes $1,000 per day, but at the salesperson's encouragement, states she makes $2,000. She gets double the money from the MCA company. She also gets a doubly high daily repayment.

Overwithholding is common, especially if you overstate your actual sales during application. But the onus is on you to contact the company and explain that you should actually be paying less than they calculated that month. Unfortunately, even if they grant you that refund, the terms of your contract won’t change going forward, so you’ll have to make these requests every month—resulting in laborious, costly accounting management.

We need more transparency about merchant cash advance loans to protect borrowers from financial ruin

Most general online research of merchant cash advances (and other names they illegally call themselves, aka “business cash advance loans” and “merchant cash advance loans”) glosses over or buries the depth of the dangers, and even guides you purposefully into them. They have no laws to follow—which means no ethics, either.

If you come across a company boasting fast funding with “no credit checks” and “no rejections,” you’ve likely encountered an MCA. Other red flags include any of the fees listed in the table above, including funding fees, late fees, and origination fees. When presented with terms like these, you’d be well advised to steer clear.

The biggest thing with SpotOn Capital is that I’m not giving investment presentations. We can fund the opening of our new business with money from our current businesses and go at our own pace. It’s super streamlined.” –Jayson Whiteside, Co-Owner, Bardo and Vana

Legitimate small business loan solutions like SpotOn Capital—focused on business health, easy application, and fast funding turnarounds—are available that will better set you up for growth and success.