How Restaurants Can Handle the Spotlight Surge

Win a culinary award? Land on that coveted best-of list? Here’s how to translate excitement into profit margins and keep standards high, with expert advice from R Town Pizza in Reno, Nevada.

Win a culinary award? Land on that coveted best-of list? Here’s how to translate excitement into profit margins and keep standards high, with expert advice from R Town Pizza in Reno, Nevada.

High-margin alcohol sales are shrinking. Here's how to maintain profits when guests buy less alcohol (and they are).

Last-minute schedule changes, overtime creep, punch errors, and payroll rework all quietly eat into your margins. Don’t treat them as separate fires. Here's how to treat them as a system that needs guardrails.

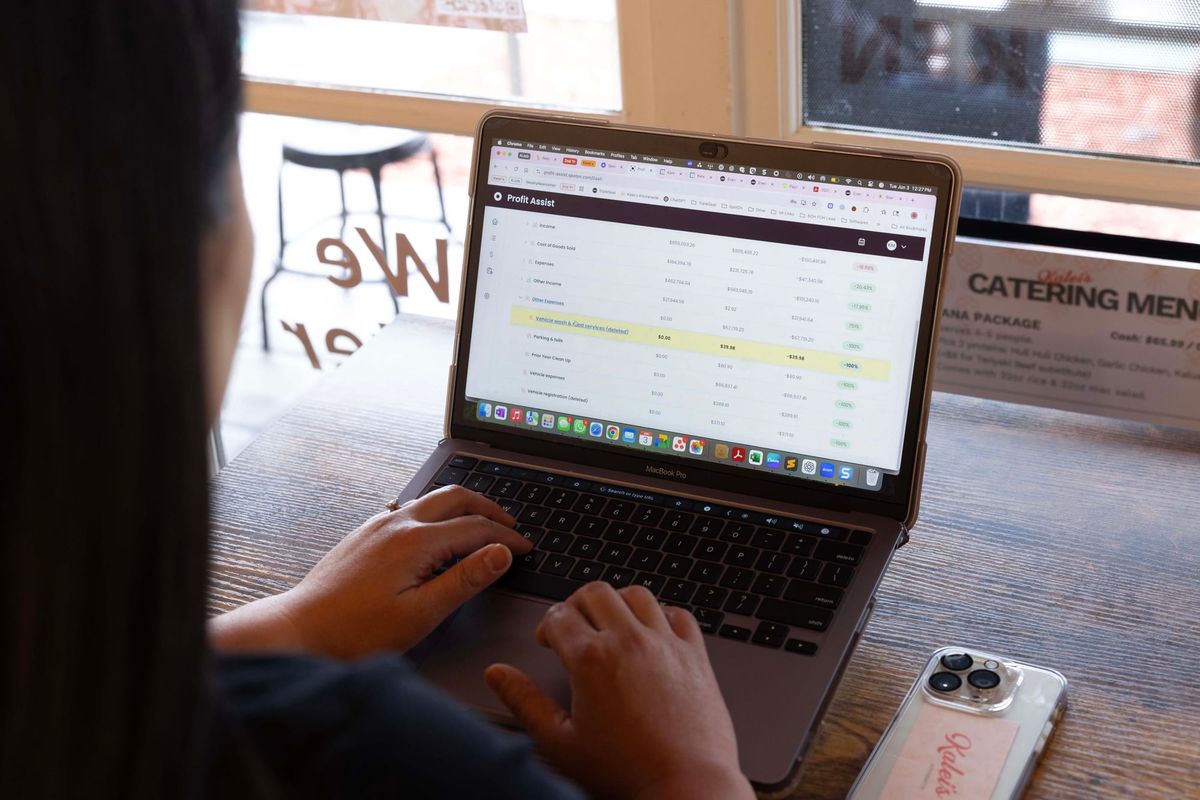

Restaurant AI should be intuitive for teams, complementary to the guest experience and impactful on your bottom line. That’s the bar.

A deep dive into restaurant marketing, covering the strategies, tools, and decisions operators need to drive real results.

Learn how to increase restaurant sales with 15 actionable strategies that help operators grow revenue sustainably and keep guests coming back.

Learn the art and science of restaurant menu creation, from concept to setting profitable prices and expert design tips.

Creating and communicating a restaurant schedule can take hours out of your day. But with the right strategies, it doesn't have to.

Learn how restaurant loans work and discover easier funding options to grow your business.

Restaurants rated SpotOn higher than Toast in major categories, cementing SpotOn as the go-to tech partner for independent operators

Make money on online orders. Learn how to keep your profits, increase online orders, control order flow, and capture guest data—without per-order commissions.

Learn how to build a restaurant tech stack that works together to streamline operations and grow your business.

Learn how to use restaurant SEO to attract more local customers, boost online visibility, and grow your business—without paying for ads.

Assess the financial health of your restaurant. Our P&L template brings together your sales and costs to calculate your profit.

Find out how popular and profitable your menu items are with our menu engineering matrix. Then learn how to modify your menu for more sales.

See how Butcher Paper BBQ used restaurant profitability analysis, labor management software, and smart restaurant technology to cut costs by 9% and reclaim the owner's time.

See how SpotOn Restaurant POS ranks on popular software review sites like G2, Trustpilot, Capterra, NerdWallet, and more.

New restaurant wins, product innovation, and strategic partnerships help operators streamline service, improve guest experiences, and protect margins.

New “instant fund” transfer feature joins DayCheck tip payouts and SpotOn Capital to give restaurant operators faster, lower-cost control over their cash flow

See how Talat Market's chef-owners used SpotOn's restaurant POS and Profit Assist to streamline operations, boost margins, and grow as a business.

On March 15, Giving Kitchen hosted Team Hidi, their biggest annual fundraiser supporting food service workers in crisis. SpotOn employees volunteered—and shared gratitude.